import pandas as pd

import numpy as np

import statsmodels.formula.api as smf

import seaborn as sns

import matplotlib.pyplot as plt

import statsmodels.api as sm5 Potential issues

Read section 3.3.3 (4, 5, & 6) of the book before using these notes.

Note that in this course, lecture notes are not sufficient, you must read the book for better understanding. Lecture notes are just implementing the concepts of the book on a dataset, but not explaining the concepts elaborately.

Let us continue with the car price prediction example from the previous chapter.

trainf = pd.read_csv('./Datasets/Car_features_train.csv')

trainp = pd.read_csv('./Datasets/Car_prices_train.csv')

testf = pd.read_csv('./Datasets/Car_features_test.csv')

testp = pd.read_csv('./Datasets/Car_prices_test.csv')

train = pd.merge(trainf,trainp)

train.head()| carID | brand | model | year | transmission | mileage | fuelType | tax | mpg | engineSize | price | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 18473 | bmw | 6 Series | 2020 | Semi-Auto | 11 | Diesel | 145 | 53.3282 | 3.0 | 37980 |

| 1 | 15064 | bmw | 6 Series | 2019 | Semi-Auto | 10813 | Diesel | 145 | 53.0430 | 3.0 | 33980 |

| 2 | 18268 | bmw | 6 Series | 2020 | Semi-Auto | 6 | Diesel | 145 | 53.4379 | 3.0 | 36850 |

| 3 | 18480 | bmw | 6 Series | 2017 | Semi-Auto | 18895 | Diesel | 145 | 51.5140 | 3.0 | 25998 |

| 4 | 18492 | bmw | 6 Series | 2015 | Automatic | 62953 | Diesel | 160 | 51.4903 | 3.0 | 18990 |

# Considering the model developed to address assumptions in the previous chapter

# Model with an interaction term and a variable transformation term

ols_object = smf.ols(formula = 'np.log(price)~(year+engineSize+mileage+mpg)**2+I(mileage**2)', data = train)

model_log = ols_object.fit()

model_log.summary()| Dep. Variable: | np.log(price) | R-squared: | 0.803 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.803 |

| Method: | Least Squares | F-statistic: | 1834. |

| Date: | Sun, 05 Feb 2023 | Prob (F-statistic): | 0.00 |

| Time: | 19:31:46 | Log-Likelihood: | -1173.8 |

| No. Observations: | 4960 | AIC: | 2372. |

| Df Residuals: | 4948 | BIC: | 2450. |

| Df Model: | 11 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Intercept | -238.2125 | 25.790 | -9.237 | 0.000 | -288.773 | -187.652 |

| year | 0.1227 | 0.013 | 9.608 | 0.000 | 0.098 | 0.148 |

| engineSize | 13.8349 | 5.795 | 2.387 | 0.017 | 2.475 | 25.195 |

| mileage | 0.0005 | 0.000 | 3.837 | 0.000 | 0.000 | 0.001 |

| mpg | -1.2446 | 0.345 | -3.610 | 0.000 | -1.921 | -0.569 |

| year:engineSize | -0.0067 | 0.003 | -2.324 | 0.020 | -0.012 | -0.001 |

| year:mileage | -2.67e-07 | 6.8e-08 | -3.923 | 0.000 | -4e-07 | -1.34e-07 |

| year:mpg | 0.0006 | 0.000 | 3.591 | 0.000 | 0.000 | 0.001 |

| engineSize:mileage | -2.668e-07 | 4.08e-07 | -0.654 | 0.513 | -1.07e-06 | 5.33e-07 |

| engineSize:mpg | 0.0028 | 0.000 | 6.842 | 0.000 | 0.002 | 0.004 |

| mileage:mpg | 7.235e-08 | 1.79e-08 | 4.036 | 0.000 | 3.72e-08 | 1.08e-07 |

| I(mileage ** 2) | 1.828e-11 | 5.64e-12 | 3.240 | 0.001 | 7.22e-12 | 2.93e-11 |

| Omnibus: | 711.515 | Durbin-Watson: | 0.498 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 2545.807 |

| Skew: | 0.699 | Prob(JB): | 0.00 |

| Kurtosis: | 6.220 | Cond. No. | 1.73e+13 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 1.73e+13. This might indicate that there are

strong multicollinearity or other numerical problems.

5.1 Outliers

An outlier is a point for which the true response (\(y_i\)) is far from the value predicted by the model. Residual plots can be used to identify outliers.

If the the response at the \(i^{th}\) observation is \(y_i\), the prediction is \(\hat{y}_i\), then the residual \(e_i\) is:

\[e_i = y_i - \hat{y_i}\]

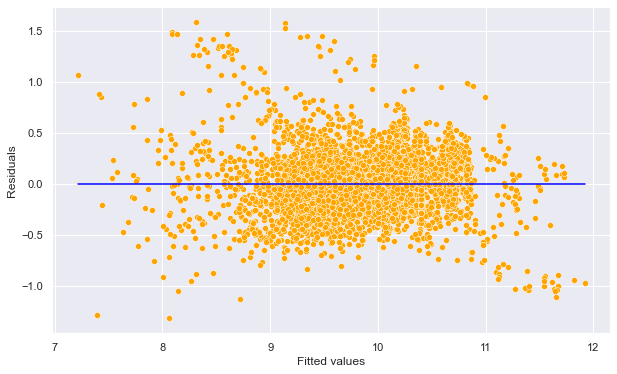

#Plotting residuals vs fitted values

sns.set(rc={'figure.figsize':(10,6)})

sns.scatterplot(x = (model_log.fittedvalues), y=(model_log.resid),color = 'orange')

sns.lineplot(x = [model_log.fittedvalues.min(),model_log.fittedvalues.max()],y = [0,0],color = 'blue')

plt.xlabel('Fitted values')

plt.ylabel('Residuals')Text(0, 0.5, 'Residuals')

Some of the errors may be high. However, it is difficult to decide how large a residual needs to be before we can consider a point to be an outlier. To address this problem, we have standardized residuals, which are defined as:

\[r_i = \frac{e_i}{RSE(\sqrt{1-h_{ii}})},\]

where \(r_i\) is the standardized residual, \(RSE\) is the residual standard error, and \(h_{ii}\) is the leverage (introduced in the next section) of the \(i^{th}\) observation.

Standardized residuals, allow the residuals to be compared on a standard scale.

Issue with standardized residuals:, If the observation corresponding to the standardized residual has a high leverage, then it will drag the regression line / plane / hyperplane towards it, thereby influencing the estimate of the residual itself.

Studentized residuals: To address the issue with standardized residuals, studentized residual for the \(i^{th}\) observation is computed as the standardized residual, but with the \(RSE\) (residual standard error) computed after removing the \(i^{th}\) observation from the data. Studentized residual, \(t_i\) for the \(i^{th}\) observation is given as:

\[t_i = \frac{e_i}{RSE_{i}(\sqrt{1-h_{ii}})},\]

where \(RSE_{i}\) is the residual standard error of the model developed on the data without the \(i^{th}\) observation.

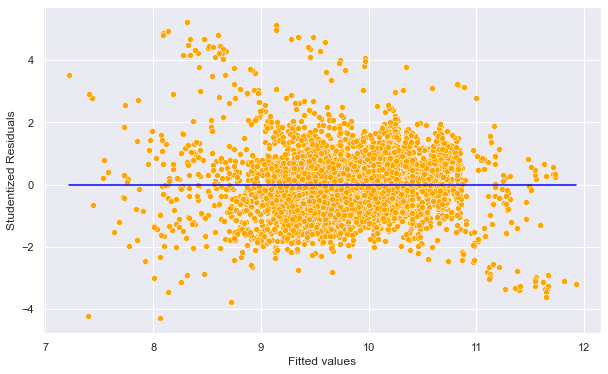

Studentized residuals follow a \(t\) distribution with \((n–p–2)\) degrees of freedom. Thus, in general, observations whose studentized residuals have a magnitude higher than 3 are potential outliers.

Let us find the studentized residuals in our car price prediction model.

#Studentized residuals

out = model_log.outlier_test()

out| student_resid | unadj_p | bonf(p) | |

|---|---|---|---|

| 0 | -1.164204 | 0.244398 | 1.0 |

| 1 | -0.801879 | 0.422661 | 1.0 |

| 2 | -1.263820 | 0.206354 | 1.0 |

| 3 | -0.614171 | 0.539130 | 1.0 |

| 4 | 0.027930 | 0.977719 | 1.0 |

| ... | ... | ... | ... |

| 4955 | -0.523361 | 0.600747 | 1.0 |

| 4956 | -0.509539 | 0.610397 | 1.0 |

| 4957 | -1.718802 | 0.085713 | 1.0 |

| 4958 | -0.077595 | 0.938153 | 1.0 |

| 4959 | -0.482388 | 0.629551 | 1.0 |

4960 rows × 3 columns

Studentized residuals are in the first column of the above table.

#Plotting studentized residuals vs fitted values

sns.scatterplot(x = (model_log.fittedvalues), y=(out.student_resid),color = 'orange')

sns.lineplot(x = [model_log.fittedvalues.min(),model_log.fittedvalues.max()],y = [0,0],color = 'blue')

plt.xlabel('Fitted values')

plt.ylabel('Studentized Residuals')Text(0, 0.5, 'Studentized Residuals')

Potential outliers: Observations whose studentized residuals have a magnitude greater than 3.

Impact of outliers: Outliers do not have a large impact on the OLS line / plane / hyperplane. However, outliers do inflate the residual standard error (RSE). RSE in turn is used to compute the standard errors of regression coefficients. As a result, statistically significant variables may appear to be insignificant, and \(R^2\) may appear to be lower.

#Number of points with absolute studentized residuals greater than 3

np.sum((np.abs(out.student_resid)>3))86Are there outliers in our example?: In the above plot, there are 86 points with absolute studentized residuals larger than 3. However, most of the predictors are significant and R-squared has a relatively high value of 80%. Thus, even if there are outliers, there is no need to remove them as it is unlikely to change the significance of individual variables. Furthermore, looking into the data, we find that the price of some of the luxury cars such as Mercedez G-class is actually much higher than average. So, the potential outliers in the data do not seem to be due to incorrect data. The high studentized residuals may be due to some deficiency in the model, such as missing predictor(s) (like car model), rather than incorrect data. Thus, we should not remove any data that has an outlying value of log(price).

Since model seems to be a variable that can explain the price of overly expensive cars, let us include it in the regression model.

#Model with an interaction term and a variable transformation term

ols_object = smf.ols(formula = 'np.log(price)~(year+engineSize+mileage+mpg)**2+I(mileage**2)+model', data = train)

model_log = ols_object.fit()

#Model summary not printed to save space

#model_log.summary()#Computing RMSE on test data with car 'model' as one of the predictors

pred_price_log2 = model_log.predict(testf)

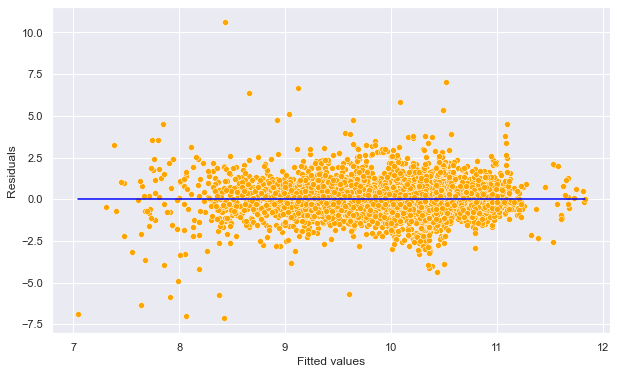

np.sqrt(((testp.price - np.exp(pred_price_log2))**2).mean())4252.20045604376#Plotting studentized residuals vs fitted values for the model with car 'model' as one of the predictors

out = model_log.outlier_test()

sns.scatterplot(x = (model_log.fittedvalues), y=(out.student_resid),color = 'orange')

sns.lineplot(x = [model_log.fittedvalues.min(),model_log.fittedvalues.max()],y = [0,0],color = 'blue')

plt.xlabel('Fitted values')

plt.ylabel('Residuals')Text(0, 0.5, 'Residuals')

#Number of points with absolute studentized residuals greater than 3

np.sum((np.abs(out.student_resid)>3))69Note the RMSE has reduced to almost half of its value as compared to the regression model without the predictor - model. Car model does help better explain the variation in price of cars! The number of points with absolute studentized residuals greater than 3 has also reduced to 69 from 86.

5.2 High leverage points

High leverage points are those with an unsual value of the predictor(s). They have a relatively higher impact on the OLS line / plane / hyperplane, as compared to the outliers.

Leverage statistic (page 99 of the book): In order to quantify an observation’s leverage, we compute the leverage statistic. A large value of this statistic indicates an observation with high leverage. For simple linear regression, \[\begin{equation} h_i = \frac{1}{n} + \frac{(x_i - \bar x)^2}{\sum_{i'=1}^{n}(x_{i'} - \bar x)^2}. \end{equation}\]

It is clear from this equation that \(h_i\) increases with the distance of \(x_i\) from \(\bar x\).The leverage statistic \(h_i\) is always between \(1/n\) and \(1\), and the average leverage for all the observations is always equal to \((p+1)/n\). So if a given observation has a leverage statistic that greatly exceeds \((p+1)/n\), then we may suspect that the corresponding point has high leverage.

Influential points: Note that if a high leverage point falls in line with the regression line, then it will not affect the regression line. However, it may inflate R-squared and increase the significance of predictors. If a high leverage point falls away from the regression line, then it is also an outlier, and will affect the regression line. The points whose presence significantly affects the regression line are called influential points. A point that is both a high leverage point and an outlier is likely to be an influential point. However, a high leverage point is not necessarily an influential point.

Source for influential points: https://online.stat.psu.edu/stat501/book/export/html/973

Let us see if there are any high leverage points in our regression model without the predictor - model.

#Model with an interaction term and a variable transformation term

ols_object = smf.ols(formula = 'np.log(price)~(year+engineSize+mileage+mpg)**2+I(mileage**2)', data = train)

model_log = ols_object.fit()

model_log.summary()| Dep. Variable: | np.log(price) | R-squared: | 0.803 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.803 |

| Method: | Least Squares | F-statistic: | 1834. |

| Date: | Sun, 05 Feb 2023 | Prob (F-statistic): | 0.00 |

| Time: | 19:31:59 | Log-Likelihood: | -1173.8 |

| No. Observations: | 4960 | AIC: | 2372. |

| Df Residuals: | 4948 | BIC: | 2450. |

| Df Model: | 11 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Intercept | -238.2125 | 25.790 | -9.237 | 0.000 | -288.773 | -187.652 |

| year | 0.1227 | 0.013 | 9.608 | 0.000 | 0.098 | 0.148 |

| engineSize | 13.8349 | 5.795 | 2.387 | 0.017 | 2.475 | 25.195 |

| mileage | 0.0005 | 0.000 | 3.837 | 0.000 | 0.000 | 0.001 |

| mpg | -1.2446 | 0.345 | -3.610 | 0.000 | -1.921 | -0.569 |

| year:engineSize | -0.0067 | 0.003 | -2.324 | 0.020 | -0.012 | -0.001 |

| year:mileage | -2.67e-07 | 6.8e-08 | -3.923 | 0.000 | -4e-07 | -1.34e-07 |

| year:mpg | 0.0006 | 0.000 | 3.591 | 0.000 | 0.000 | 0.001 |

| engineSize:mileage | -2.668e-07 | 4.08e-07 | -0.654 | 0.513 | -1.07e-06 | 5.33e-07 |

| engineSize:mpg | 0.0028 | 0.000 | 6.842 | 0.000 | 0.002 | 0.004 |

| mileage:mpg | 7.235e-08 | 1.79e-08 | 4.036 | 0.000 | 3.72e-08 | 1.08e-07 |

| I(mileage ** 2) | 1.828e-11 | 5.64e-12 | 3.240 | 0.001 | 7.22e-12 | 2.93e-11 |

| Omnibus: | 711.515 | Durbin-Watson: | 0.498 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 2545.807 |

| Skew: | 0.699 | Prob(JB): | 0.00 |

| Kurtosis: | 6.220 | Cond. No. | 1.73e+13 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 1.73e+13. This might indicate that there are

strong multicollinearity or other numerical problems.

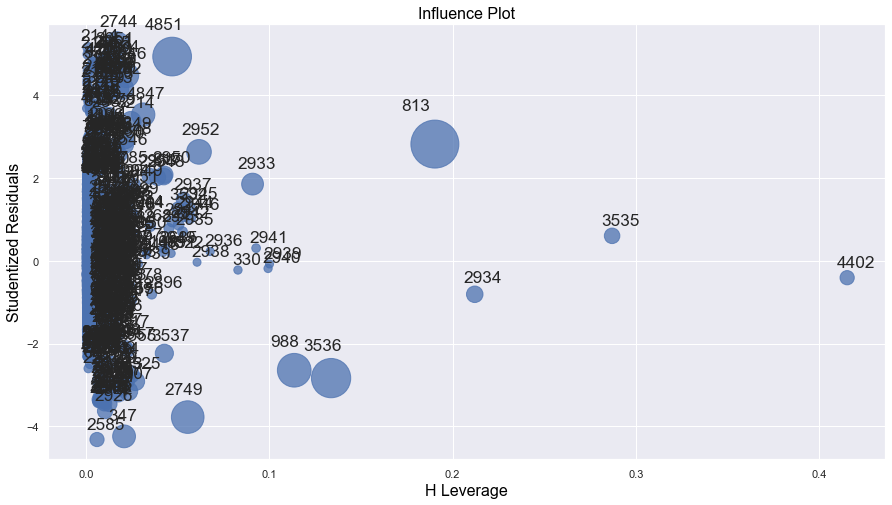

#Computing the leverage statistic for each observation

influence = model_log.get_influence()

leverage = influence.hat_matrix_diag#Visualizng leverage against studentized residuals

sns.set(rc={'figure.figsize':(15,8)})

sm.graphics.influence_plot(model_log);

Let us identify the high leverage points in the data, as they may be affecting the regression line if they are outliers as well, i.e., if they are influential points. Note that there is no defined threshold for a point to be classified as a high leverage point. Some statisticians consider points having twice the average leverage as high leverage points, some consider points having thrice the average leverage as high leverage points, and so on.

out = model_log.outlier_test()#Average leverage of points

average_leverage = (model_log.df_model+1)/model_log.nobs

average_leverage0.0024193548387096775Let us consider points having four times the average leverage as high leverage points.

#We will remove all observations that have leverage higher than the threshold value.

high_leverage_threshold = 4*average_leverage#Number of high leverage points in the dataset

np.sum(leverage>high_leverage_threshold)1975.3 Influential points

Observations that are both high leverage points and outliers are influential points that may affect the regression line. Let’s remove these influential points from the data and see if it improves the model prediction accuracy on test data.

#Dropping influential points from data

train_filtered = train.drop(np.intersect1d(np.where(np.abs(out.student_resid)>3)[0],

(np.where(leverage>high_leverage_threshold)[0])))train_filtered.shape(4921, 11)#Number of points removed as they were influential

train.shape[0]-train_filtered.shape[0]39We removed 39 influential data points from the training data.

#Model after removing the influential observations

ols_object = smf.ols(formula = 'np.log(price)~(year+engineSize+mileage+mpg)**2+I(mileage**2)', data = train_filtered)

model_log = ols_object.fit()

model_log.summary()| Dep. Variable: | np.log(price) | R-squared: | 0.830 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.829 |

| Method: | Least Squares | F-statistic: | 2173. |

| Date: | Sun, 29 Jan 2023 | Prob (F-statistic): | 0.00 |

| Time: | 01:26:25 | Log-Likelihood: | -775.51 |

| No. Observations: | 4921 | AIC: | 1575. |

| Df Residuals: | 4909 | BIC: | 1653. |

| Df Model: | 11 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Intercept | -262.7743 | 24.455 | -10.745 | 0.000 | -310.717 | -214.832 |

| year | 0.1350 | 0.012 | 11.148 | 0.000 | 0.111 | 0.159 |

| engineSize | 16.6645 | 5.482 | 3.040 | 0.002 | 5.917 | 27.412 |

| mileage | 0.0008 | 0.000 | 5.945 | 0.000 | 0.001 | 0.001 |

| mpg | -1.1217 | 0.324 | -3.458 | 0.001 | -1.758 | -0.486 |

| year:engineSize | -0.0081 | 0.003 | -2.997 | 0.003 | -0.013 | -0.003 |

| year:mileage | -3.927e-07 | 6.5e-08 | -6.037 | 0.000 | -5.2e-07 | -2.65e-07 |

| year:mpg | 0.0005 | 0.000 | 3.411 | 0.001 | 0.000 | 0.001 |

| engineSize:mileage | -4.566e-07 | 3.86e-07 | -1.183 | 0.237 | -1.21e-06 | 3e-07 |

| engineSize:mpg | 0.0071 | 0.000 | 16.202 | 0.000 | 0.006 | 0.008 |

| mileage:mpg | 7.29e-08 | 1.68e-08 | 4.349 | 0.000 | 4e-08 | 1.06e-07 |

| I(mileage ** 2) | 1.418e-11 | 5.29e-12 | 2.683 | 0.007 | 3.82e-12 | 2.46e-11 |

| Omnibus: | 631.414 | Durbin-Watson: | 0.553 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 1851.015 |

| Skew: | 0.682 | Prob(JB): | 0.00 |

| Kurtosis: | 5.677 | Cond. No. | 1.73e+13 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 1.73e+13. This might indicate that there are

strong multicollinearity or other numerical problems.

Note that we obtain a higher R-sqauared value of 83% as compared to 80% with the complete data. Removing the influential points helped obtain a better model fit. However, that may also happen just by reducing observations.

#Computing RMSE on test data

pred_price_log = model_log.predict(testf)

np.sqrt(((testp.price - np.exp(pred_price_log))**2).mean())8820.685844070766The RMSE on test data has also reduced. This shows that some of the influential points were impacting the regression line. With those points removed, the model better captures the general trend in the data.

5.4 Collinearity

Collinearity refers to the situation when two or more predictor variables have a high linear association. Linear association between a pair of variables can be measured by the correlation coefficient. Thus the correlation matrix can indicate some potential collinearity problems.

5.4.1 Why and how is collinearity a problem

(Source: page 100-101 of book)

The presence of collinearity can pose problems in the regression context, since it can be difficult to separate out the individual effects of collinear variables on the response.

Since collinearity reduces the accuracy of the estimates of the regression coefficients, it causes the standard error for \(\hat \beta_j\) to grow. Recall that the t-statistic for each predictor is calculated by dividing \(\hat \beta_j\) by its standard error. Consequently, collinearity results in a decline in the \(t\)-statistic. As a result, in the presence of collinearity, we may fail to reject \(H_0: \beta_j = 0\). This means that the power of the hypothesis test—the probability of correctly detecting a non-zero coefficient—is reduced by collinearity.

5.4.2 How to measure collinearity/multicollinearity

(Source: page 102 of book)

Unfortunately, not all collinearity problems can be detected by inspection of the correlation matrix: it is possible for collinearity to exist between three or more variables even if no pair of variables has a particularly high correlation. We call this situation multicollinearity. Instead of inspecting the correlation matrix, a better way to assess multicollinearity is to compute the variance inflation factor (VIF). The VIF is variance inflation factor the ratio of the variance of \(\hat \beta_j\) when fitting the full model divided by the variance of \(\hat \beta_j\) if fit on its own. The smallest possible value for VIF is 1, which indicates the complete absence of collinearity. Typically in practice there is a small amount of collinearity among the predictors. As a rule of thumb, a VIF value that exceeds 5 or 10 indicates a problematic amount of collinearity.

The estimated variance of the coefficient \(\beta_j\), of the \(j^{th}\) predictor \(X_j\), can be expressed as:

\[\hat{var}(\hat{\beta_j}) = \frac{(\hat{\sigma})^2}{(n-1)\hat{var}({X_j})}.\frac{1}{1-R^2_{X_j|X_{-j}}},\]

where \(R^2_{X_j|X_{-j}}\) is the \(R\)-squared for the regression of \(X_j\) on the other covariates (a regression that does not involve the response variable \(Y\)).

In case of simple linear regression, the variance expression in the equation above does not contain the term \(\frac{1}{1-R^2_{X_j|X_{-j}}}\), as there is only one predictor. However, in case of multiple linear regression, the variance of the estimate of the \(j^{th}\) coefficient (\(\hat{\beta_j}\)) gets inflated by a factor of \(\frac{1}{1-R^2_{X_j|X_{-j}}}\) (Note that in the complete absence of collinearity, \(R^2_{X_j|X_{-j}}=0\), and the value of this factor will be 1).

Thus, the Variance inflation factor, or the VIF for the estimated coefficient of the \(j^{th}\) predictor \(X_j\) is:

\[\begin{equation} VIF(\hat \beta_j) = \frac{1}{1-R^2_{X_j|X_{-j}}} \end{equation}\]

#Correlation matrix

train.corr()| carID | year | mileage | tax | mpg | engineSize | price | |

|---|---|---|---|---|---|---|---|

| carID | 1.000000 | 0.006251 | -0.001320 | 0.023806 | -0.010774 | 0.011365 | 0.012129 |

| year | 0.006251 | 1.000000 | -0.768058 | -0.205902 | -0.057093 | 0.014623 | 0.501296 |

| mileage | -0.001320 | -0.768058 | 1.000000 | 0.133744 | 0.125376 | -0.006459 | -0.478705 |

| tax | 0.023806 | -0.205902 | 0.133744 | 1.000000 | -0.488002 | 0.465282 | 0.144652 |

| mpg | -0.010774 | -0.057093 | 0.125376 | -0.488002 | 1.000000 | -0.419417 | -0.369919 |

| engineSize | 0.011365 | 0.014623 | -0.006459 | 0.465282 | -0.419417 | 1.000000 | 0.624899 |

| price | 0.012129 | 0.501296 | -0.478705 | 0.144652 | -0.369919 | 0.624899 | 1.000000 |

Let us compute the Variance Inflation Factor (VIF) for the four predictors.

X = train[['mpg','year','mileage','engineSize']]X.columns[1:]Index(['year', 'mileage', 'engineSize'], dtype='object')from statsmodels.stats.outliers_influence import variance_inflation_factor

from statsmodels.tools.tools import add_constant

X = add_constant(X)

vif_data = pd.DataFrame()

vif_data["feature"] = X.columns

for i in range(len(X.columns)):

vif_data.loc[i,'VIF'] = variance_inflation_factor(X.values, i)

print(vif_data) feature VIF

0 const 1.201579e+06

1 mpg 1.243040e+00

2 year 2.452891e+00

3 mileage 2.490210e+00

4 engineSize 1.219170e+00As all the values of VIF are close to one, we do not have the problem of multicollinearity in the model. Note that the VIF of year and mileage is relatively high as they are the most correlated.

Q1: Why is the VIF of the constant so high?

Q2: Why do we need to include the constant while finding the VIF?

5.4.3 Manual computation of VIF

#Manually computing the VIF for year

ols_object = smf.ols(formula = 'year~mpg+engineSize+mileage', data = train)

model_log = ols_object.fit()

model_log.summary()| Dep. Variable: | year | R-squared: | 0.592 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.592 |

| Method: | Least Squares | F-statistic: | 2400. |

| Date: | Mon, 30 Jan 2023 | Prob (F-statistic): | 0.00 |

| Time: | 02:49:19 | Log-Likelihood: | -10066. |

| No. Observations: | 4960 | AIC: | 2.014e+04 |

| Df Residuals: | 4956 | BIC: | 2.017e+04 |

| Df Model: | 3 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Intercept | 2018.3135 | 0.140 | 1.44e+04 | 0.000 | 2018.039 | 2018.588 |

| mpg | 0.0095 | 0.002 | 5.301 | 0.000 | 0.006 | 0.013 |

| engineSize | 0.1171 | 0.037 | 3.203 | 0.001 | 0.045 | 0.189 |

| mileage | -9.139e-05 | 1.08e-06 | -84.615 | 0.000 | -9.35e-05 | -8.93e-05 |

| Omnibus: | 2949.664 | Durbin-Watson: | 1.161 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 63773.271 |

| Skew: | -2.426 | Prob(JB): | 0.00 |

| Kurtosis: | 19.883 | Cond. No. | 1.91e+05 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 1.91e+05. This might indicate that there are

strong multicollinearity or other numerical problems.

#VIF for year

1/(1-0.592)2.4509803921568625Note that year and mileage have a high linear correlation. Removing one of them should decrease the standard error of the coefficient of the other, without significanty decrease R-squared.

ols_object = smf.ols(formula = 'price~mpg+engineSize+mileage+year', data = train)

model_log = ols_object.fit()

model_log.summary()| Dep. Variable: | price | R-squared: | 0.660 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.660 |

| Method: | Least Squares | F-statistic: | 2410. |

| Date: | Tue, 07 Feb 2023 | Prob (F-statistic): | 0.00 |

| Time: | 21:39:45 | Log-Likelihood: | -52497. |

| No. Observations: | 4960 | AIC: | 1.050e+05 |

| Df Residuals: | 4955 | BIC: | 1.050e+05 |

| Df Model: | 4 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Intercept | -3.661e+06 | 1.49e+05 | -24.593 | 0.000 | -3.95e+06 | -3.37e+06 |

| mpg | -79.3126 | 9.338 | -8.493 | 0.000 | -97.620 | -61.006 |

| engineSize | 1.218e+04 | 189.969 | 64.107 | 0.000 | 1.18e+04 | 1.26e+04 |

| mileage | -0.1474 | 0.009 | -16.817 | 0.000 | -0.165 | -0.130 |

| year | 1817.7366 | 73.751 | 24.647 | 0.000 | 1673.151 | 1962.322 |

| Omnibus: | 2450.973 | Durbin-Watson: | 0.541 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 31060.548 |

| Skew: | 2.045 | Prob(JB): | 0.00 |

| Kurtosis: | 14.557 | Cond. No. | 3.83e+07 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 3.83e+07. This might indicate that there are

strong multicollinearity or other numerical problems.

Removing mileage from the above regression.

ols_object = smf.ols(formula = 'price~mpg+engineSize+year', data = train)

model_log = ols_object.fit()

model_log.summary()| Dep. Variable: | price | R-squared: | 0.641 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.641 |

| Method: | Least Squares | F-statistic: | 2951. |

| Date: | Tue, 07 Feb 2023 | Prob (F-statistic): | 0.00 |

| Time: | 21:40:00 | Log-Likelihood: | -52635. |

| No. Observations: | 4960 | AIC: | 1.053e+05 |

| Df Residuals: | 4956 | BIC: | 1.053e+05 |

| Df Model: | 3 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Intercept | -5.586e+06 | 9.78e+04 | -57.098 | 0.000 | -5.78e+06 | -5.39e+06 |

| mpg | -101.9120 | 9.500 | -10.727 | 0.000 | -120.536 | -83.288 |

| engineSize | 1.196e+04 | 194.848 | 61.392 | 0.000 | 1.16e+04 | 1.23e+04 |

| year | 2771.1844 | 48.492 | 57.147 | 0.000 | 2676.118 | 2866.251 |

| Omnibus: | 2389.075 | Durbin-Watson: | 0.528 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 26920.051 |

| Skew: | 2.018 | Prob(JB): | 0.00 |

| Kurtosis: | 13.675 | Cond. No. | 1.41e+06 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 1.41e+06. This might indicate that there are

strong multicollinearity or other numerical problems.

Note that the standard error of the coefficient of year has reduced from 73 to 48, without any large reduction in R-squared.

5.4.4 When can we overlook multicollinearity?

The severity of the problems increases with the degree of the multicollinearity. Therefore, if there is only moderate multicollinearity (5 < VIF < 10), we may overlook it.

Multicollinearity affects only the standard errors of the coefficients of collinear predictors. Therefore, if multicollinearity is not present for the predictors that we are particularly interested in, we may not need to resolve it.

Multicollinearity affects the standard error of the coefficients and thereby their \(p\)-values, but in general, it does not influence the prediction accuracy, except in the case that the coefficients are so unstable that the predictions are outside of the domain space of the response. If our sole aim is prediction, and we don’t wish to infer the statistical significance of predictors, then we may avoid addressing multicollinearity. “The fact that some or all predictor variables are correlated among themselves does not, in general, inhibit our ability to obtain a good fit nor does it tend to affect inferences about mean responses or predictions of new observations, provided these inferences are made within the region of observations” - Neter, John, Michael H. Kutner, Christopher J. Nachtsheim, and William Wasserman. “Applied linear statistical models.” (1996): 318.